Global spending on security solutions has been increased by 9.4% from 2017. IDC new global spending report data shows that global spending on security related hardware, software and related services to reach approx $103.1 billion in 2019. Adaptation of new technologies like cloud, IoT, AI boosting organizations growth but also brings cyber security threats, Organizations are increasing their budget on security solutions and according to report spending on security solutions will go continuously for the next several years.

According to the Worldwide Semiannual Security Spending Guide from IDC, worldwide spending on security solutions will achieve a compound annual growth rate (CAGR) of 9.2% over the 2018-2022 forecast period and total $133.8 billion in 2022.

The three industries that will spending the most on security solutions in 2019 – banking, discrete manufacturing, and federal/central government – will invest more than $30 billion combined.

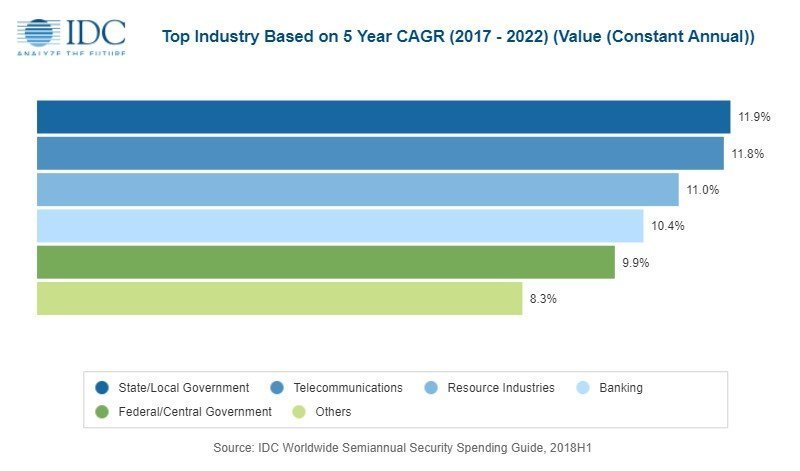

Three other industries (process manufacturing, professional services, and telecommunications) will each see spending greater than $6.0 billion this year. The industries that will experience the fastest spending on security solutions growth over the forecast period will be state/local government (11.9% CAGR), telecommunications (11.8% CAGR), and the resource industries (11.3% CAGR). This security solutions spending growth will make telecommunications the fourth largest industry for security spending in 2022 while state/local government will move into the sixth position ahead of professional services.

Spending on Security Solutions Industry Wise

“When examining the largest and fastest growing segments for security, we see a mix of industries – such as banking and government – that are charged with guarding highly sensitive information in regulated environments. In addition, information-based organizations like professional services firms and telcos are ramping up spending. But regardless of industry, these technologies remain an investment priority in virtually all enterprises, as delivering a sense of security is everyone’s business,” said Jessica Goepfert, program vice president, Customer Insights and Analysis.

Managed security services will be the largest technology category in 2019 with firms spending on security solutions more than $21 billion for around-the-clock monitoring and management of security operations centers. Managed security services will also be the largest category of spending for each of the top five industries this year.

The second largest technology category in 2019 will be network security hardware, which includes unified threat management, firewalls, and intrusion detection and prevention technologies. The third and fourth largest investment categories will be integration services and endpoint security software. The technology categories that will see the fastest spending growth over the forecast will be managed security services (14.2% CAGR), security analytics, intelligence, response and orchestration software (10.6% CAGR), and network security software (9.3% CAGR).

“The security landscape is changing rapidly, and organizations continue to struggle to maintain their own in-house security solutions and staff. As a result, organizations are turning to managed security service providers (MSSPs) to deliver a wide span of security capabilities and consulting services, which include predicative threat intelligence and advanced detection and analysis expertise that are necessary to overcome the security challenges happening today as well as prepare organizations against future attacks,” said Martha Vazquez, senior research analyst, Infrastructure Services.

From a geographic perspective, the United States will be the single largest market for security solutions with spending forecast to reach $44.7 billion in 2019. Two industries – discrete manufacturing and the federal government – will account for nearly 20% of the U.S. total. The second largest market will be China where security purchases by three industries — state/local government, telecommunications, and central government – will comprise 45% of the national total. Japan and the UK are the next two largest markets with security spending led by the consumer sector and the banking industry respectively.

“While the U.S. and Western Europe will deliver two-thirds of the total security spend this year, the largest growth in security solutions spending will be seen in China, Asia/Pacific (excluding Japan and China), and Latin America, each with double-digit CAGRs over the five-year forecast period,” said Karen Massey, research manager, Customer Insights & Analysis.

Large (500-1000 employees) and very large businesses (more than 1000 employees) will be responsible for roughly two thirds of all spending on security solutions in 2019. These two segments will also see the strongest spending growth over the forecast with CAGRs of 11.1% for large businesses and 9.4% for very large businesses. Medium (100-499 employees) and small businesses (10-99 employees) will spend nearly $26 billion combined on security solutions in 2019. Consumers are forecast to spend nearly $5.7 billion on security this year.